As an administrative lawyer with a background in applied physics and technology management, I analyze legal risks not just through documents, but through the lens of structural logic and physical evidence.

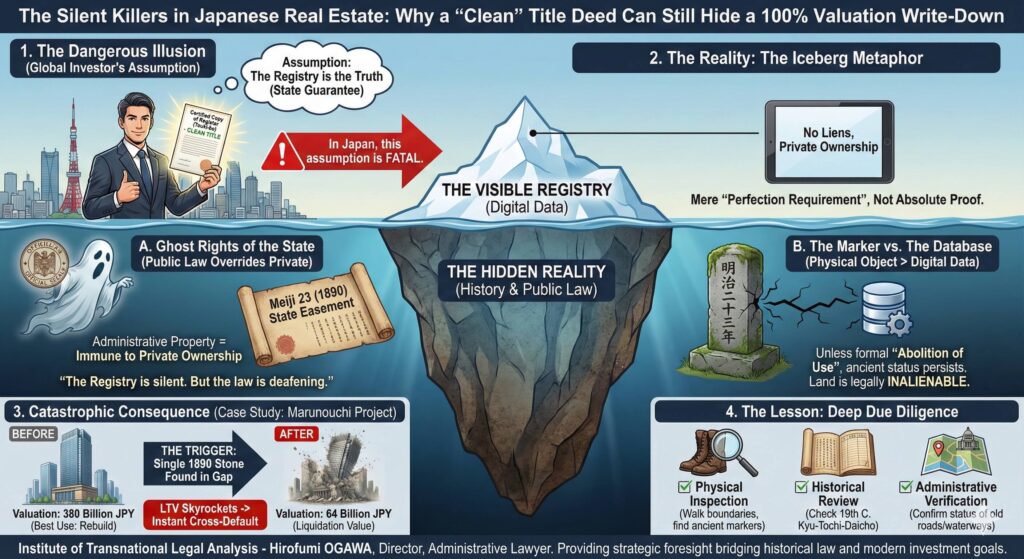

The Silent Killers in Japanese Real Estate (Part 1)

Why a “Clean” Title Deed Can Still Hide a 100% Valuation Write-Down

If you are a global investor looking at Tokyo’s prime real estate, you likely operate on a fundamental assumption: “The Registry is the Truth.”

In jurisdictions like the UK or under the Torrens system, the land registry provides a state guarantee of title. If a risk isn’t listed on the document, for all legal purposes, it doesn’t exist. You hire a top-tier law firm, they pull the Certified Copy of the Register (Touki-bo), confirm there are no liens or encumbrances, and you sign the deal.

In Japan, this assumption can be a fatal mistake.

In my recent economic novel, The Man Who Slaughters the Red Dragon, I depict a scenario where a global fund targets a prime office building in Marunouchi, Tokyo. The deal—valued at over 300 billion JPY—collapses not because of market shifts or interest rates, but because of a single, moss-covered stone block hidden in a 50cm gap between buildings.

Here is why the Japanese registry creates a dangerous illusion for the uninitiated.

1. The “Ghost” Rights of the State

In Japan, the Real Property Registration Act acts merely as a “perfection requirement” (Taiko Yoken) against third parties under the Civil Code. It is not absolute proof of ownership validity.

More terrifyingly, public law often overrides private registration. In the novel, the fatal flaw was a “Government-Retained Right” (State Easement) established in Meiji 23 (1890) for a railway project. Because this land is classified as “Administrative Property” (Gyosei Zaisan) under the State Property Act, it is legally immune to private ownership or prescription. Even if the registry shows the land is private, and even if it has been traded privately for 100 years, the State’s right remains absolute.

The registry is silent. But the law is deafening.

2. The Marker Stone vs. The Database

In the story, the protagonist discovers a granite marker stone from 1890 on the site. This physical object carries more legal weight than the digital registry data. Why? Because under Japanese administrative law, unless there is a formal “Abolition of Use” (Yoto Haishi), public status persists indefinitely.

The global investor assumed that because the registry was clean, the development rights (air rights) could be transferred. They calculated the building’s value based on a “Best and Highest Use” scenario of rebuilding a skyscraper. However, the existence of that single stone meant the land was legally “inalienable.” The redevelopment permit was voided.

The result? The valuation crashed from a 380 billion JPY development project to a 64 billion JPY liquidation value in seconds. The LTV (Loan-to-Value) ratio skyrocketed, triggering an instant cross-default on global loans.

3. The Lesson for Global Investors

Japan is a country where layers of history—Meiji, Taisho, Showa—are stacked upon each other. The modern digital registry is just the top layer of paint. Deep Due Diligence in Japan requires more than checking the Touki-bo. It requires:

• Physical Inspection: Walking the boundary lines to look for ancient government markers.

• Historical Review: Checking old land ledgers (Kyu-Tochi-Daicho) from the 19th century.

• Administrative Verification: Confirming the status of public roads and waterways that may not appear on maps.

Do not let the “Illusion of the Register” blind you. In Tokyo, the most dangerous risks are the ones that have been sleeping in the soil for 130 years.

Are You Performing “Deep Due Diligence” on Your Japanese Assets?

In a market as complex as Tokyo, technical compliance is not enough. You need strategic, analytical foresight that bridges the gap between historical administrative law and modern investment goals.

Institute of Transnational Legal Analysis Providing high-stakes risk assessment and regulatory navigation for global institutional investors.

Hirofumi OGAWA Director, Administrative Lawyer (License No. 25100579) B.S. & M.S. in Applied Physics, Master in Management of Technology (MOT)

[Contact for Consultation: LinkedIn Message or Email Address]

The Silent Killers in Japanese Real Estate (Part 2): The Physicality of Governance

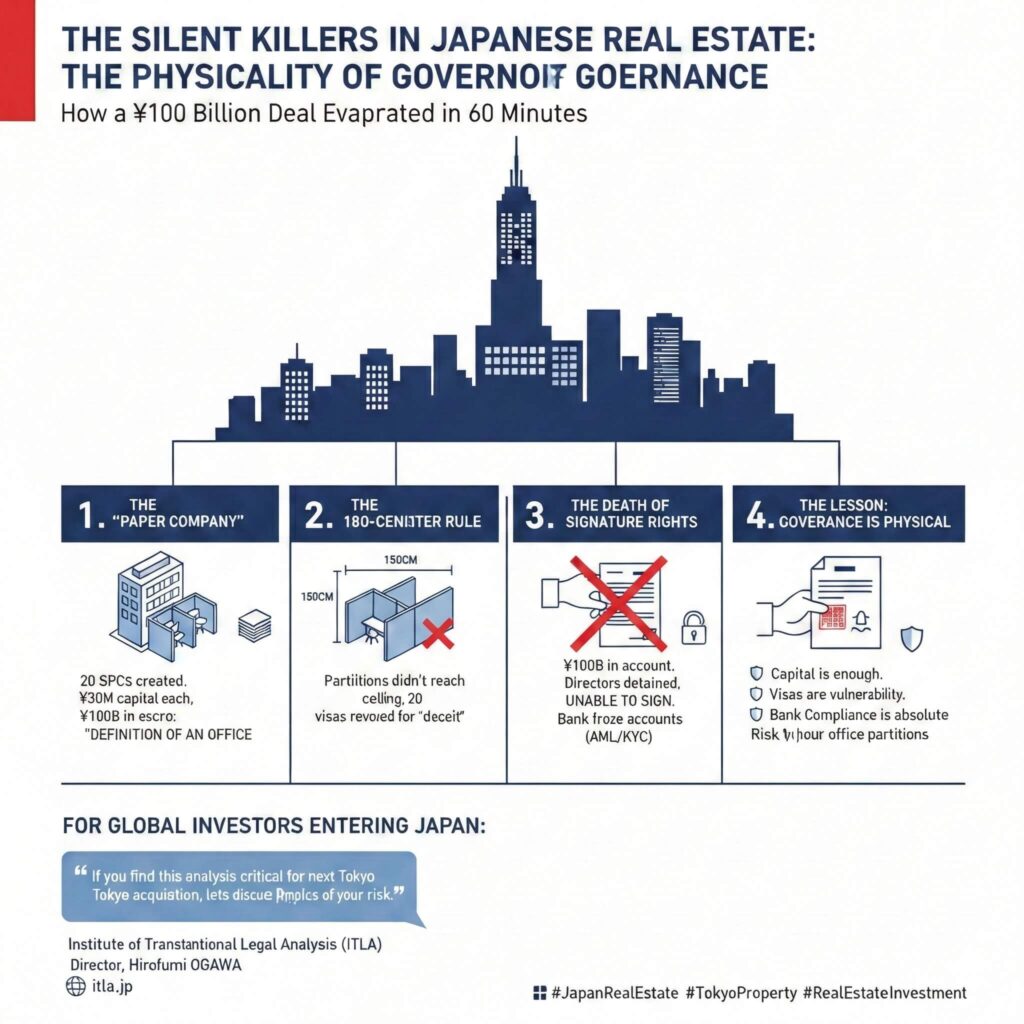

Capital Has No Nationality, But Directors Do: How a 100 Billion JPY Deal Evaporated in 60 Minutes

In the world of cross-border real estate, we tend to view Special Purpose Companies (SPCs) as abstract containers—legal fictions designed to hold assets and optimize tax. In jurisdictions like the Cayman Islands or Delaware, a director can be a mere signature on a PDF.

In Japan, however, corporate governance has a stubborn, unavoidable “physicality.”

In Part 2 of my analysis based on the economic novel The Man Who Slaughters the Red Dragon, I explore how a sophisticated 100 billion JPY acquisition collapsed not because of a lack of funds, but because of a lack of “physical existence” required by Japanese law.

1. The “Paper Company”

In the story, the antagonist, Zhang, sets up 20 separate SPCs to fragment ownership. To staff these, he brings in 20 subordinates using the “Business Manager” (Keiei-Kanri) visa. On paper, everything was flawless: 30 million JPY capital per company and 100 billion JPY ready in escrow.

But they missed one bureaucratic detail: The Definition of an “Office.”

2. The 180-Centimeter Rule

Under Japanese immigration regulations, a company must have a physical, independent office space. Zhang’s 20 SPCs were partitioned into booths in one large room.

The flaw? The partitions did not reach the ceiling. Under strict interpretation, this was not 20 offices; it was one room. The “physical facility” requirement was not met. Hours before the closing, the Immigration Bureau raided the office, and all 20 visas were revoked for “obtaining status by deceit.”

3. The Death of Signature Rights

This is the nightmare scenario. In Japan, a loan drawdown requires the physical seal or signature of a valid representative.

- The Capital was there: 100 billion JPY sat in the account.

- The Hand was missing: Because the visas were revoked, the directors lost their legal standing. They were detained and physically unable to sign.

The result? The bank instantly froze the accounts under AML/KYC protocols. The deal failed because the legal personality of the borrower ceased to function. The registry is silent. But the physical wall is deafening.

4. The Lesson: Governance is Physical

For global investors entering Japan:

- Capital is not enough: You need a physically compliant governance structure.

- Visas are vulnerability: Immigration status is a single point of failure.

- Bank Compliance is absolute: They will freeze a deal at the 11th hour if the “Representative’s Status” is in question.

In Tokyo, the most dangerous risks aren’t just in the documents—they are in the height of your office partitions.

“If you find this analysis critical for your next Tokyo acquisition, let’s discuss the physics of your risk.”

Institute of Transnational Legal Analysis (ITLA) Director, Hirofumi OGAWA 🌐 itla.jp

#JapanRealEstate #TokyoProperty #RealEstateInvestment

The Silent Killers in Japanese Real Estate (Part 3): The Global Contagion

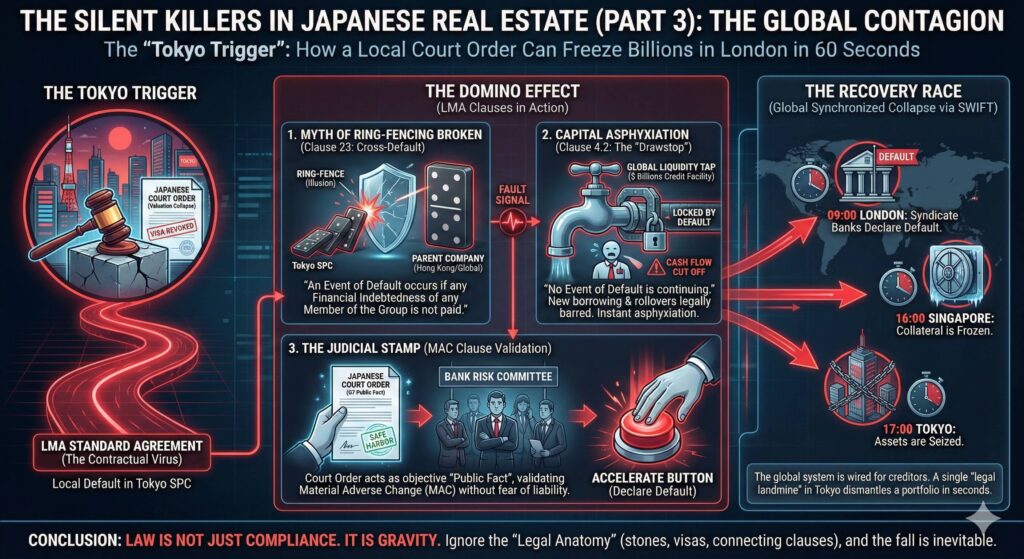

The “Tokyo Trigger”: How a Local Court Order Can Freeze Billions in London in 60 Seconds

In Part 1 and Part 2 of this series, we explored how archaic Japanese property laws (Meiji-era easements) and strict immigration rules can physically halt a real estate project. Some investors might think: “So what? If a single SPC in Tokyo fails, it’s a ring-fenced loss. The parent company is safe.”

This is the most dangerous misconception in global finance.

In my economic novel, The Man Who Slaughters the Red Dragon, the protagonist uses a specific legal mechanism to turn a local default in Tokyo into a global fatal wound for a Hong Kong conglomerate. The weapon is not a Japanese law, but the standard template used in almost all international syndicated loans: The LMA (Loan Market Association) Agreement.

Here is how the “Tokyo Trigger” works.

1. The Myth of Ring-Fencing (LMA Clause 23)

Global investors often believe that Special Purpose Companies (SPCs) insulate the parent company from liability. However, if the parent company has borrowed funds under LMA standard terms (common in Hong Kong, London, and Singapore), the definition of “Group” in the contract is critical.

Clause 23 (Cross-Default) typically states:

“An Event of Default occurs if any Financial Indebtedness of any Member of the Group is not paid when due.”

In the story, when the Tokyo SPC fails to execute a payment due to the loss of its representative (visa revocation) or asset value collapse (court order), it triggers an instant “Event of Default” for the parent company in Hong Kong. The “ring-fence” is an illusion. The virus travels through the contract.

2. The Asphyxiation of Capital (The “Drawstop”)

The true terror of the LMA agreement isn’t just the demand for repayment; it’s the “Drawstop” (Clause 4.2).

Most real estate funds operate on “Rollover Loans”—borrowing new money to pay off old short-term debt. However, Clause 4.2 imposes a strict condition precedent for any new borrowing:

“No Event of Default is continuing.”

The moment the default flag is raised in Tokyo (e.g., at 5:00 PM JST), the parent company in Hong Kong is legally barred from drawing down any new funds or rolling over existing debts. Even if they have a $1 billion credit facility, the bank’s computer system automatically locks the liquidity tap. The company doesn’t die from debt; it dies from asphyxiation (lack of cash flow).

3. The Judicial Stamp (The MAC Clause)

Banks are often hesitant to call a default based on vague rumors. They fear lender liability. This is where the “Material Adverse Change” (MAC) clause comes into play.

In the novel, the protagonist uses a Japanese Court Order (confirming the valuation collapse of the Tokyo asset) as a “Public Fact.” He sends this court document to the legal counsels of the syndicate banks in London. For a bank’s risk committee, a court order from a G7 country is the ultimate “safe harbor.” It validates the MAC clause objectively. It gives them the legal cover to push the “Accelerate” button without fear of being sued.

4. The Recovery Race

Once Acceleration is declared, the timeline shifts from weeks to seconds. It becomes a “Recovery Race.”

• 09:00 London: Syndicate banks declare default.

• 17:00 Tokyo: Assets are seized.

• 16:00 Singapore: Collateral is frozen.

The global financial system is wired to protect creditors, not borrowers. A single “legal landmine” stepped on in Marunouchi, Tokyo, transmits a signal through the SWIFT network that can dismantle a global portfolio before the sun sets.

Conclusion to the Series

Investing in Japan offers tremendous opportunities, but it requires a specific kind of “Legal Anatomy.” You must look beyond the spreadsheet. You must look at the stones in the ground, the visas in the passports, and the specific clauses in your loan agreements that link them all together.

In the world of cross-border investment, Law is not just compliance. It is gravity. Ignore it, and the fall is inevitable.

——————————————————————————–

(End of Series. Based on the novel “The Man Who Slaughters the Red Dragon” – A Financial Thriller.)

#LMA #GlobalInvestment #JapanRealEstate #ITLA