Why Corporate Bankruptcy Often Means Personal Ruin: A Legal Analysis of the Ryomo Transport Incident in Japan

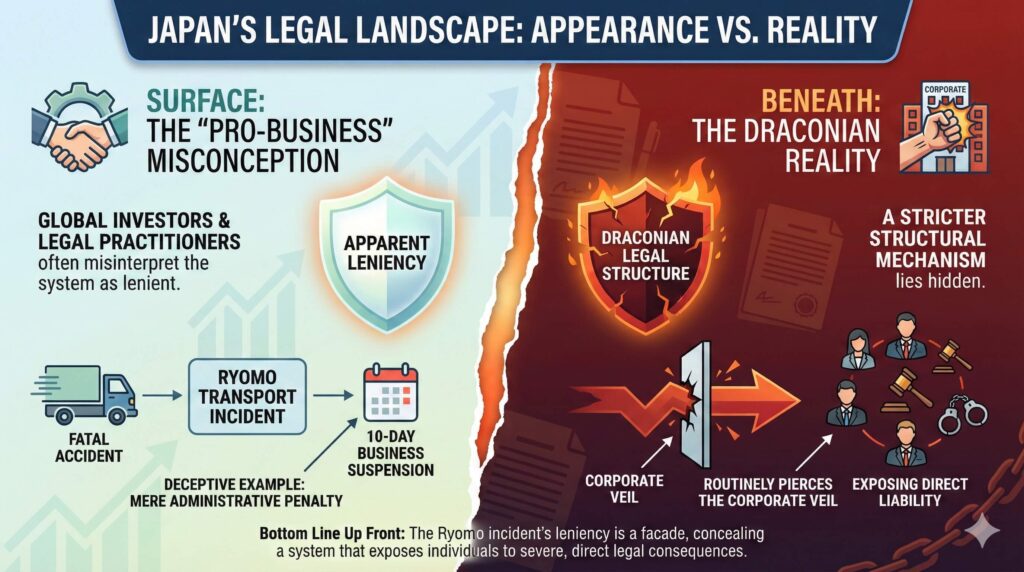

Bottom Line Up Front: Global investors and legal practitioners often misinterpret the Japanese legal landscape as “pro-business” due to the apparent leniency of administrative penalties. The recent Ryomo Transport incident—where a fatal accident resulted in a mere 10-day business suspension—serves as a deceptive example.

Beneath this administrative surface lies a draconian reality: Japanese law possesses structural mechanisms that routinely pierce the corporate veil, exposing directors to unlimited personal liability.

This article argues three critical points:

1. Statutory Direct Liability (Article 429): Unlike the US/UK “Alter Ego” doctrine which requires a high burden of proof (fraud/sham), Japan’s Companies Act Article 429 allows third parties (victims/creditors) to sue directors directly for “gross negligence” regarding internal controls.

2. Institutionalized Personal Guarantees (Ren-tai Hosho): The pervasive banking practice of requiring CEOs to sign Joint and Several Guarantees functionally nullifies the concept of limited liability for SMEs, linking corporate insolvency directly to personal bankruptcy.

3. The “Economic Death Penalty”: While the administrative state imposes minor temporal sanctions (suspensions), the private sector (banks and supply chains) executes an immediate “economic death penalty” through cross-default clauses and forfeiture of the benefit of time triggered by such sanctions.

Read this if: You are a foreign director, investor, or legal counsel operating in Japan, assuming your assets are shielded by the corporate entity. They may not be.

1. Introduction: The Ryomo Paradox – “Leniency” as a Trap

The Optical Illusion of the “10-Day Suspension”

On January 21, 2025, the Kanto District Transport Bureau handed down a seemingly mild penalty to Ryomo Transport, a trucking company responsible for a drunk-driving accident that claimed three lives: a 10-day business suspension and a cumulative suspension of vehicle use.

To a Wall Street attorney or a City of London solicitor, this penalty appears woefully inadequate—a “slap on the wrist” that implies a lack of regulatory enforcement. In the United States, a similar incident involving gross negligence (systematic failure of alcohol checks) would likely trigger Punitive Damages in the range of tens of millions of dollars, effectively liquidating the company immediately.

However, this “leniency” is an optical illusion generated by the rigid formalism of the Motor Truck Transportation Business Act and its “Point System” algorithm. The Japanese administrative state does not wield the discretionary power to issue an immediate “Out of Service” order based on imminent hazard, unlike the US Department of Transportation (DOT). Instead, it strictly follows a pre-determined calculation: Violation Count × Severity = Penalty Days.

The Real Sanction: Private Sector Enforcement

The true terror of the Japanese system lies not in the administrative penalty itself, but in what that penalty triggers within the private legal ecosystem. The moment the “10-day suspension” is gazetted, it acts as a material breach signal across the company’s entire commercial and financial network.

1. Commercial Ostracism: Major shippers, bound by strict compliance covenants, will execute termination clauses without notice (Civil Code Art. 541 implication). In Japan’s high-context trust society, losing a key contract due to a “compliance scandal” is rarely a temporary setback; it is often a permanent exclusion from the market.

2. Financial Acceleration: Banks will invoke the “Forfeiture of Benefit of Time” (Acceleration Clause) in loan agreements. The administrative sanction serves as an objective “Event of Default,” allowing lenders to demand immediate full repayment of principal.

The Thinner Veil

Consequently, the company faces an “Economic Death Penalty” executed not by the state, but by the market. But the destruction does not stop at the corporate entity. Unlike in Common Law jurisdictions, where the Corporate Veil is a robust shield protecting executives from personal financial ruin (absent fraud), the Japanese veil is structurally thin.

Through the mechanisms of Companies Act Article 429 and the ubiquitous Joint and Several Guarantee, the liability travels upstream, piercing the corporate shell and attaching directly to the personal assets of the directors. The Ryomo Transport incident is not merely a traffic accident case; it is a stark warning of how quickly “Limited Liability” can evaporate in the Japanese legal environment.

Complying with the source material and the “Monster of Intellect” persona, I will write Block 2.

Here, we dissect the unique Japanese legal mechanism that contractually destroys the concept of limited liability for SME owners: the Joint and Several Guarantee (Ren-tai Hosho).

2. “Ren-tai Hosho” (Joint and Several Guarantee) – The Institutionalized Piercing

The Ubiquity of the “Human Collateral”

In the United States or the UK, a bank loan to a corporation is generally non-recourse to its directors, absent specific “bad boy” carve-outs or personal guarantees limited to specific assets. In Japan, however, the Joint and Several Guarantee (Ren-tai Hosho) is not an exception; for decades, it has been the banking standard.

For Small and Medium Enterprises (SMEs) like Ryomo Transport, the CEO does not merely manage the entity; they are the credit enhancement. By stamping their personal seal on a Ren-tai Hosho agreement, the director voluntarily strips away the protection of the corporate veil, placing their personal home, savings, and future earnings on the altar of corporate solvency.

Legal Analysis: Why “Joint and Several” is Lethal

To understand the lethality of this instrument, one must distinguish between a “Simple Guarantee” (Hosho) and a “Joint and Several Guarantee” (Ren-tai Hosho) under the Civil Code of Japan.

A Simple Guarantor enjoys two powerful statutory defenses:

- Defense of Notice (Saikoku no Koben – Civil Code Art. 452): The guarantor can refuse to pay until the creditor has first demanded payment from the principal debtor.

- Defense of Inquiry/Excussion (Kensaku no Koben – Civil Code Art. 453): Even if the creditor demands payment, the guarantor can refuse if they can prove the principal debtor has assets that can be easily executed upon.

However, the Joint and Several Guarantee explicitly waives these protections. Civil Code Article 454 states:

“A guarantor who has agreed to guarantee the obligation jointly and severally with the principal debtor shall not have the rights provided in the preceding two Articles [Defense of Notice and Defense of Inquiry].”

Furthermore, under Civil Code Article 456, if there are multiple guarantors, a simple guarantor would enjoy the Benefit of Division (Buntan no Rieki), being liable only for their pro-rata share. A Joint and Several Guarantor has no such benefit; they are liable for 100% of the debt, regardless of the number of co-guarantors.

The Practical Consequence: In the event of a default (triggered, for example, by a bank’s acceleration clause following an administrative suspension), the bank is legally entitled to bypass the company’s assets entirely and immediately seize the CEO’s personal bank accounts and foreclose on their family residence.

The “Desperation” Incentive

This legal structure creates a perverse incentive structure foreign to Western governance. In the West, a CEO might declare Chapter 11 bankruptcy to restructure. In Japan, corporate bankruptcy for an SME almost invariably triggers the personal bankruptcy of the owner.

This context is essential to understanding the Ryomo Transport incident. The “15 violations” found by the audit—cutting corners on safety, ignoring alcohol checks, reworking drivers to the bone—are not merely symptoms of poor management. They are often symptoms of existential terror. When the “death of the company” equals the “social and financial death of the individual,” compliance costs become the first casualty in the battle for survival.

While the Ren-tai Hosho pierces the veil via contract, Japanese law possesses an even more dangerous weapon that requires no contract at all—a statutory provision that allows third-party victims to strike directly at the director’s personal assets.

Complying with the blueprint and maintaining the analytical depth required for international legal practitioners, I will write Block 3.

Here, we examine the Japanese statutory mechanism that terrifies foreign directors once they understand its full scope: Companies Act Article 429.

3. The Sword of Damocles – Companies Act Article 429

The Structural Bypass of the Corporate Entity

In Anglo-American jurisprudence, a director’s fiduciary duty is owed primarily to the corporation and its shareholders. If a director is negligent, the corporation (or shareholders via a derivative suit) sues the director. Third parties—such as accident victims or unpaid creditors—generally cannot sue directors personally unless they can pierce the corporate veil by proving the company was a sham or used for fraud (“Alter Ego” theory).

Japan flips this paradigm. It offers third parties a statutory “bypass road” directly to the director’s personal bank account. This is Article 429, Paragraph 1 of the Companies Act.

(Liability to Third Parties) Article 429 (1): If Officers, etc. were willful or grossly negligent in the performance of their duties, such Officers, etc. shall be liable to compensate third parties for damages arising as a result thereof.

“Gross Negligence” vs. The Business Judgment Rule

The terrifying aspect for directors is the threshold: “Gross Negligence” (Ju-kashitsu). While the “Business Judgment Rule” exists in Japanese case law, it is significantly weaker when matters of regulatory compliance and safety are involved.

In the case of Ryomo Transport, the Kanto District Transport Bureau officially certified 15 distinct violations, including the systematic failure to conduct roll calls (tenko), falsification of records, and failure to manage driver health. To a Japanese judge, these findings are not merely evidence of a “bad business culture.” They constitute a breach of the director’s statutory duty to establish a functioning Internal Control System (Companies Act Art. 362(4)(vi)).

Under Japanese judicial precedent, a representative director who allows such a state of lawlessness to persist is deemed to have committed “Gross Negligence” (essentially, a reckless disregard for their supervisory duties).

The “Direct” Liability Consequence

The legal mechanics here are lethal:

- No Derivative Requirement: The victims’ families do not need to wait for the company to sue the director. They sue the director directly as the primary defendant.

- Joint and Several Liability: Under Article 430, if the company is also liable (which it is, under the Civil Code and Automobile Liability Security Act), the director and the company are jointly and severally liable.

- The Result: If Ryomo Transport cannot pay the estimated 300–500 million yen in damages (due to the credit freeze described in Block 1), the victims can execute judgment against the President’s personal real estate, securities, and savings for the full amount.

Unlike in the US, where “piercing the veil” is an extraordinary remedy for extraordinary fraud, Article 429 is a routine weapon in the Japanese litigator’s arsenal. It turns a compliance failure into a personal financial apocalypse.

Complying with the blueprint and the “Monster of Intellect” persona, I will write Block 4 and Block 5, concluding the article.

Here, we dissect the comparative legal theory that baffles Western observers and provide the final strategic warning for global investors.

4. Comparative Legal Analysis – Common Law vs. Japanese Law

Why Western Logic Fails in Tokyo Courts

For a Director from a Common Law jurisdiction (US, UK, Australia), the liability structure described above is often counter-intuitive. They operate under the assumption that the corporate entity is distinct from its officers, and that “Piercing the Corporate Veil” is an extraordinary remedy reserved for extraordinary malfeasance.

In Japan, however, the veil is not “pierced” by judicial exception; it is bypassed by statutory design.

1. The “Alter Ego” Doctrine vs. Statutory Shortcut

- US/UK (Common Law): To hold a director personally liable for a company’s torts or debts to third parties, a plaintiff generally must prove that the company was a “sham,” an “alter ego” of the director, or that the corporate form was used specifically to perpetrate a fraud. This is a high evidentiary bar. Negligence in supervision is rarely enough to touch personal assets.

- Japan (Civil Law): Companies Act Article 429 does not require the plaintiff to prove the company is a sham. It only requires proof that the director failed in their duty with “willfulness or gross negligence.” The “15 violations” in the Ryomo case serve as objective proof of this failure. The statute functions as a “Statutory Shortcut” that eliminates the need for complex veil-piercing arguments.

2. The Duty of Oversight: A Trap for “Silent” Directors

A fatal misconception among foreign or non-executive directors in Japan is the belief that “I was not in charge of that specific division (e.g., safety), so I am not liable.”

Japanese courts have established strict precedents regarding the Duty of Oversight (Kanshi-Gimu). A representative director cannot delegate away their ultimate responsibility for legal compliance. If a subordinate (like the operations manager in the Ryomo case) commits repeated violations, the court asks: “Did the Director construct an internal control system sufficient to detect and prevent this?” If the answer is “No”—evidenced by the lack of alcohol checks or roll calls—the Director is deemed grossly negligent by omission. In Japan, “doing nothing” is a legally actionable act of destruction against one’s own personal wealth.

5. Conclusion – The Hidden Cost of Doing Business in Japan

The “Double Jeopardy” of Japanese Management

The Ryomo Transport incident elucidates the brutal architecture of the Japanese sanctioning regime. On the surface, the state appears lenient, imposing a mere “10-day administrative suspension.” However, this leniency is deceptive. The administrative penalty acts as a triggering event for a private-sector execution mechanism that is far more efficient and ruthless than any government fine.

The sequence is algorithmic:

- Administrative Trigger: 10-day suspension (Objective Event of Default).

- Commercial Freeze: Customers terminate contracts; cash flow stops.

- Financial Acceleration: Banks strip the “Benefit of Time” and demand full repayment.

- Corporate Insolvency: The company collapses.

- Personal Ruin: The Ren-tai Hosho and Article 429 transfer the remaining massive liabilities directly to the Director’s personal estate.

Strategic Warning for Global Investors

For global entities entering the Japanese market, the lessons are clear:

- “Settlement” is not a Safety Net: Unlike in the US, where regulatory fines can often be settled without admitting liability (and covered by insurance), Japanese administrative punishments are public and absolute. They destroy the “Trust” required to maintain banking covenants.

- D&O Insurance Limitations: Directors must scrutinize their D&O policies. Japanese policies often exclude coverage for damages arising from “criminal acts” or “intentional violations of law.” If the court rules that “gross negligence” regarding drunk driving equates to “willful misconduct” (a likely scenario), the insurance payout may be zero.

- The Price of Governance: Compliance in Japan is not merely a regulatory cost; it is an asset protection strategy for the individual director.

Final Verdict: The “10 days” given to Ryomo Transport was not a reprieve. It was a countdown. In the Japanese legal ecosystem, a company does not need to be fined into bankruptcy by the government. It simply needs to be marked as “unclean” by the regulator. Once that mark is applied, the market—and the mechanisms of personal liability—will finish the job with terrifying efficiency.

(End of Article)

コメント